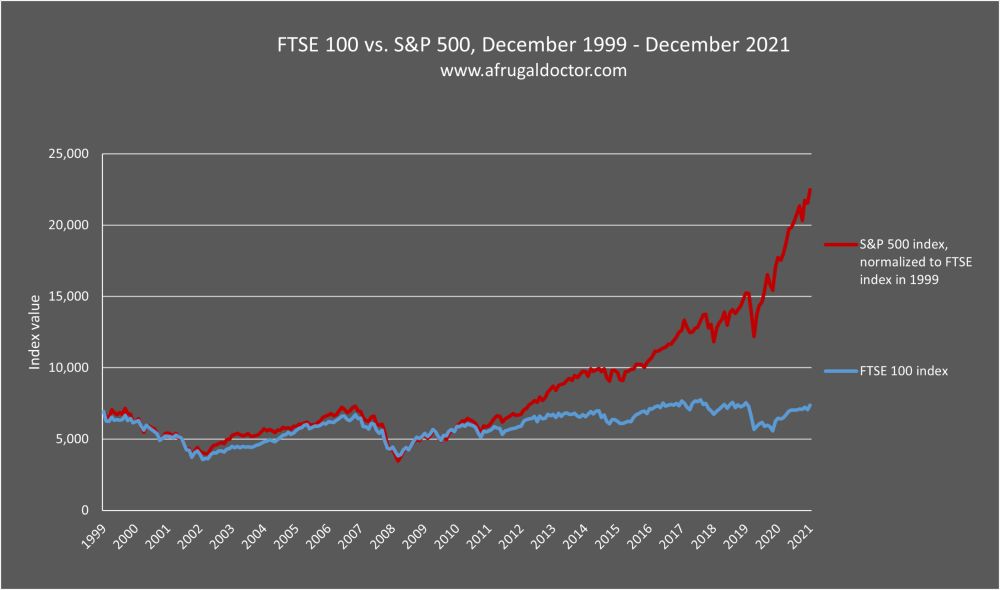

I mean I can be your case study, I have savings in the low five figures and they're just in a highish interest savings account on Monzo because 1) I have absolutely no idea what else you should do with it 2) I assume any investment means you may lose money instead, which I don't want