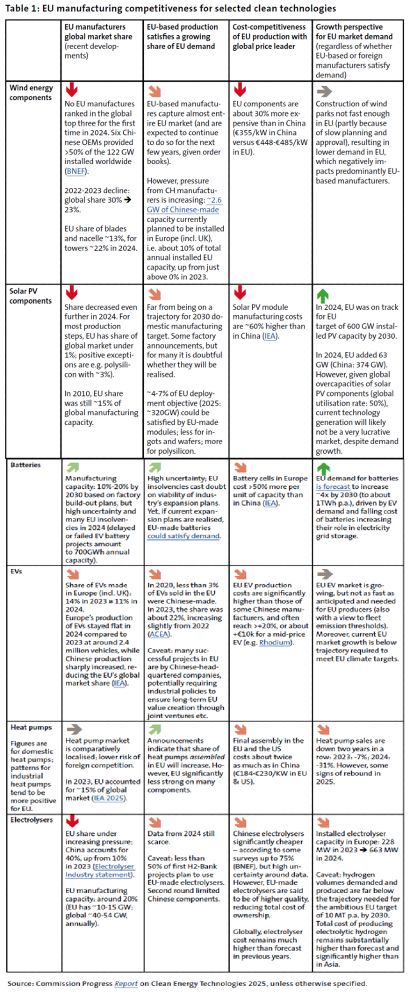

The CID implementation needs to be very bold, given the massive challenges of the sectors. On clean tech, Chinese products are often MUCH cheaper. And EU-based producers continue to lose market share in the EU and globally. The chart shows the recent developments (higher quality in PDF): (5/n)