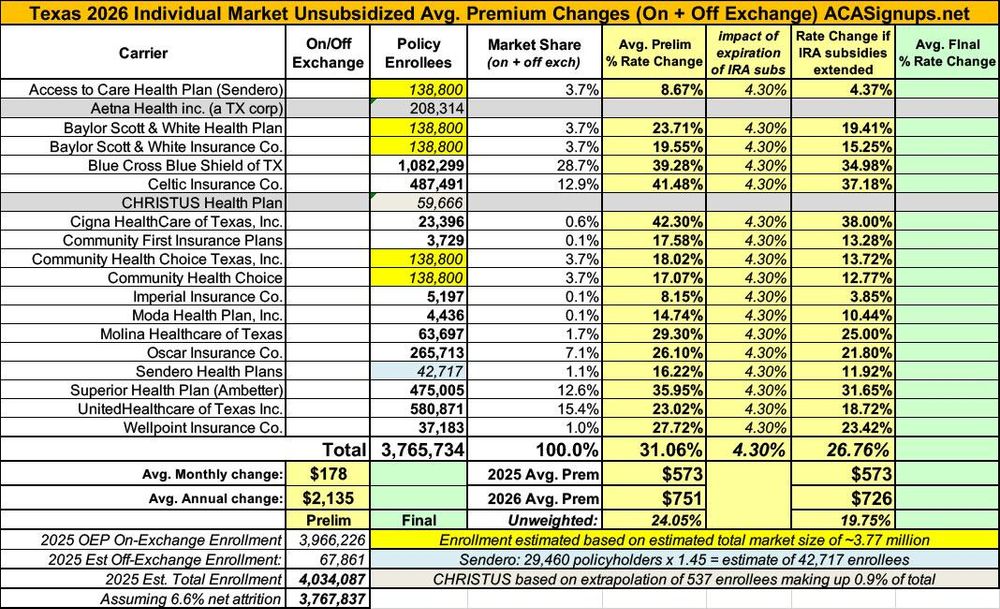

Texas carriers plan on increasing average premiums by a collective 31% statewide... ...except, again, for Aetna, which is definitely dropping out, as is CHRISTUS (at least I think they are). ~250,000 full-price enrollees are looking at paying ~31% more starting in January.