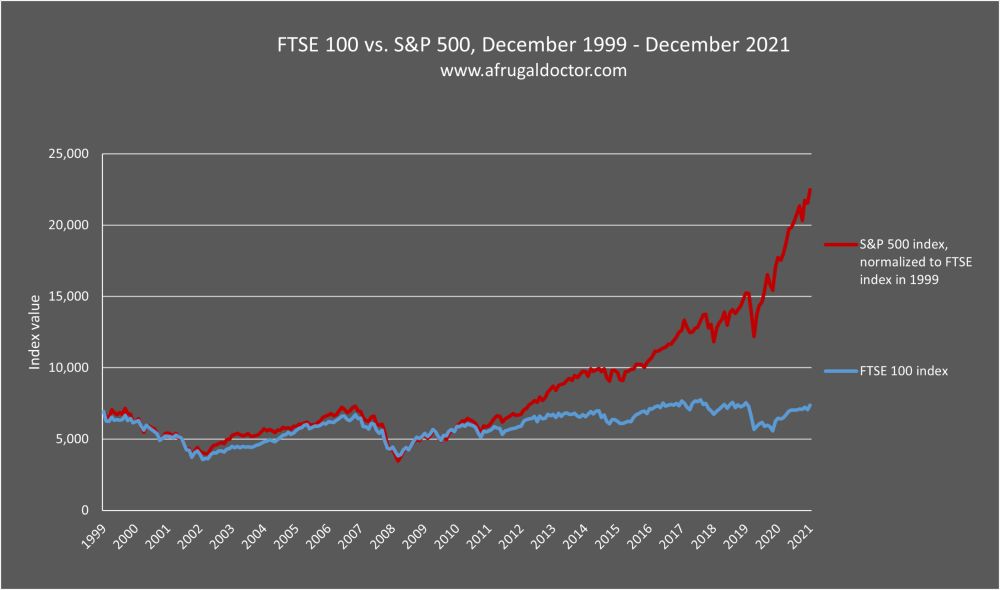

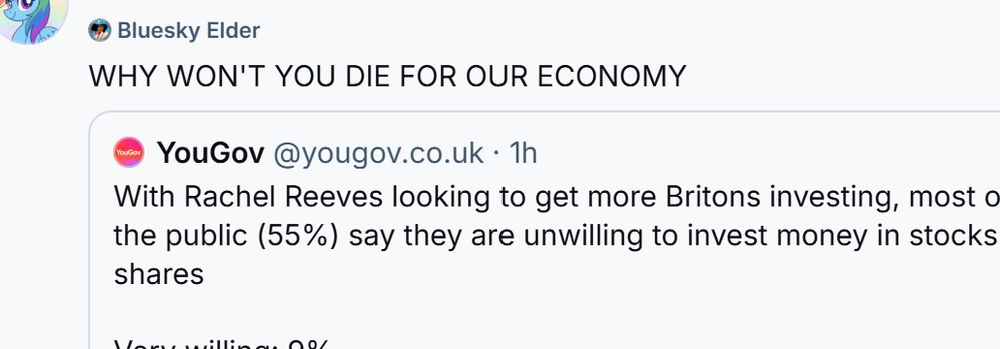

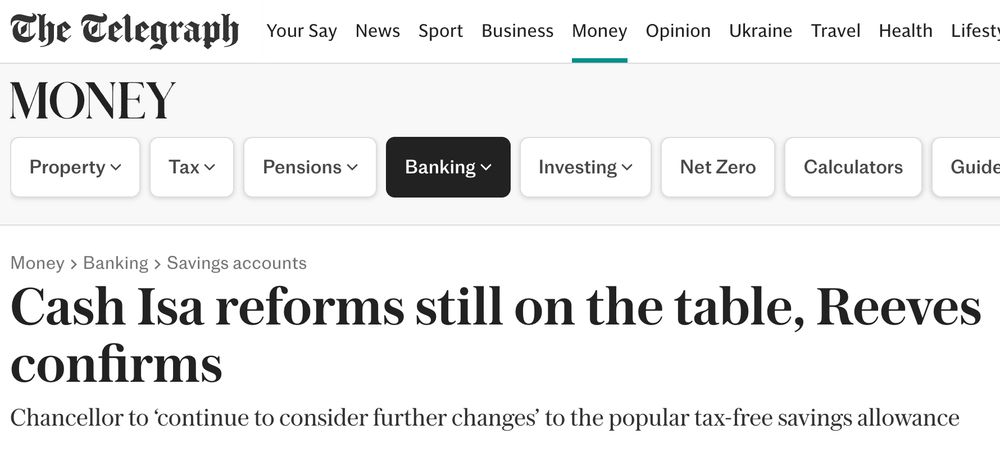

Why did I check the quote tweets on this? I knew they were going to depress me, just wall to wall people who are going to be poorer than they should be in old age who think that “invest more in stocks and shares ISAs” is some kind of spiv’s charter and not, you know, important advice.